Wondering how to peek at your credit score without risking your financial privacy or credit standing? Checking your score safely is straightforward with trusted methods that avoid scams and hard inquiries.

This guide covers simple, global steps, top tools, and tips to keep your credit health in check effortlessly.

What is a Credit Score Check?

A credit score check lets you view a number summarizing your creditworthiness, based on your borrowing history, payments, and debts.

Scores range from poor to excellent and help lenders assess risk, but you can access yours without applying for new credit.

Safe checks use “soft inquiries” that don’t ding your score, unlike hard pulls from loan applications.

Key Benefits of Safe Checking

Regularly monitoring your score spots errors, tracks progress, and prevents fraud early.

- Fraud alerts: Catch unauthorized accounts before they escalate.

- Improvement insights: See how payments or debt reduction boost your score.

- No cost or risk: Free options exist globally without impacting your rating.

- Peace of mind: Stay informed for big moves like loans or rentals.

These perks empower better financial decisions without hidden fees or data risks.

Best Safe Methods and Tools

Stick to official bureaus and reputable free services for secure access. Here’s how:

- AnnualCreditReport.com equivalents: In many countries, government-backed sites offer free annual reports from major bureaus (like Equifax, Experian, TransUnion). Check weekly where available—no score impact.

- Credit Karma or similar: Free scores from TransUnion/Equifax, with alerts and tips. Available in multiple countries; soft pulls only.

- Direct from bureaus: Experian or Equifax sites provide free scores and reports. Log in securely for ongoing monitoring.

- Bank/credit card portals: Many issuers (e.g., Chase, Barclays globally) share your FICO score monthly via statements or apps.

Always verify sites use HTTPS and avoid unsolicited emails promising “free scores.”

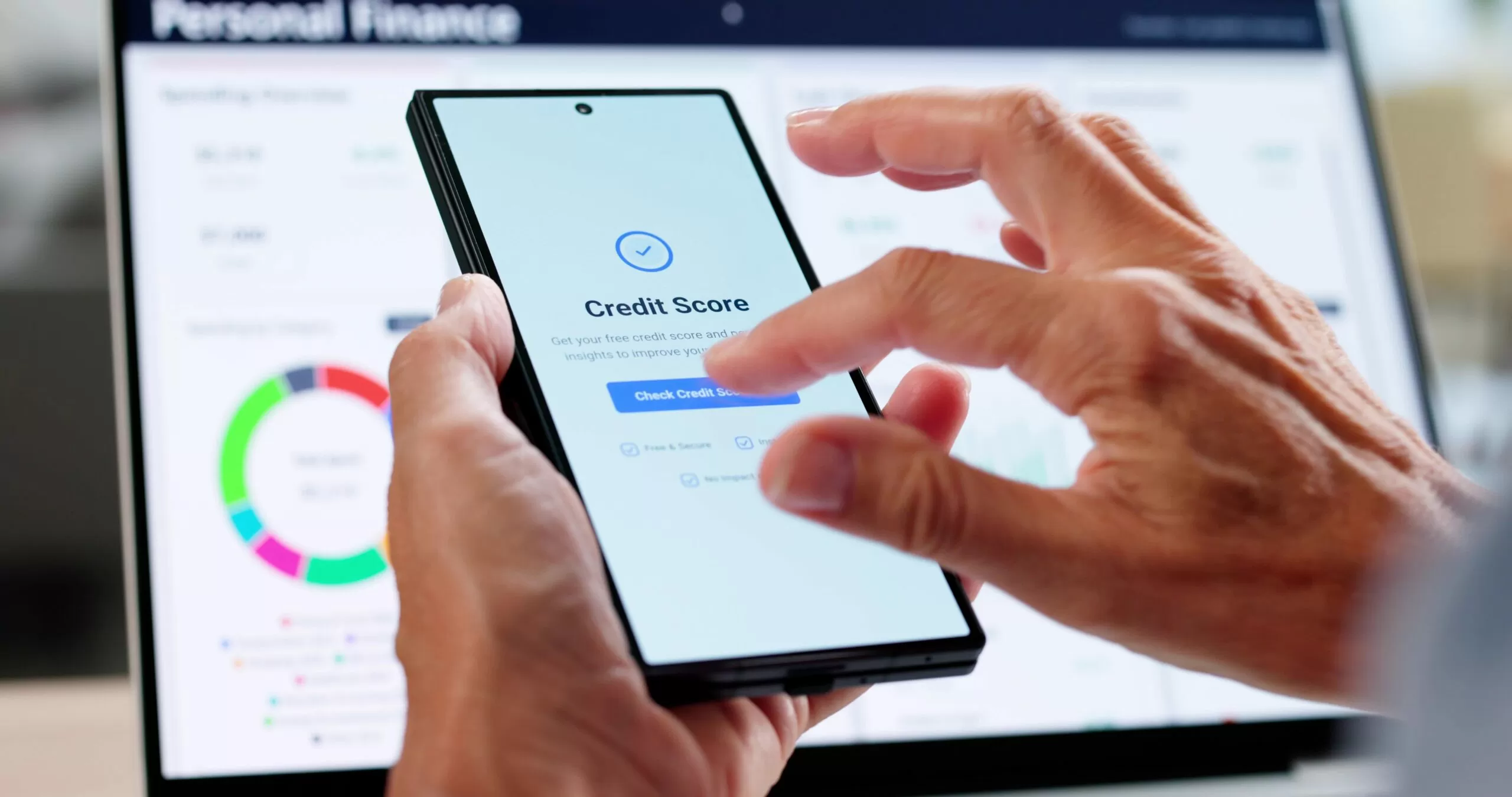

This image shows a typical credit dashboard from a safe app, highlighting score, trends, and alerts for easy tracking.

Comparison of Popular Options

Choose based on your location—prioritize bureau-direct for accuracy.

Pros and Cons

Pros:

- Free or low-cost with no credit hit.

- Real-time fraud detection saves money long-term.

- Educational tools help build better habits.

Cons:

- Scores vary by model (FICO vs. VantageScore).

- Not all countries have free universal access.

- Requires creating secure accounts with personal info.

Balanced use minimizes downsides while maximizing value.

Practical Tips for Safe Checking

- Use strong, unique passwords and enable two-factor authentication on all accounts.

- Check monthly, but not obsessively—focus on changes.

- Dispute errors directly via bureau sites; provide proof like payment receipts.

- Set up alerts for new inquiries or address changes.

- For global users, search your country’s credit bureau (e.g., CIC in Canada, Schufa in Germany) for local free options.

- Avoid “score booster” apps promising instant fixes—they’re often scams.

Real-life example: Sarah noticed a mystery account via Credit Karma alerts, froze it, and saved her score from dropping 50 points.

Frequently Asked Questions (FAQs)

How often can I safely check my credit score?

As often as services allow—weekly or more via free tools—since soft inquiries don’t affect it.

Will checking my score lower it?

No, if using soft-pull methods like bureau sites or apps. Only loan applications do.

Are there truly free ways worldwide?

Yes, via official bureaus or banks in many places; frequency varies by country.

What if I spot an error on my report?

Contact the bureau online with details—they must investigate free of charge.

Can I check without an account?

Limited options exist via statements, but apps offer the fullest free views.

Conclusion

Safe credit score checks are easy with official tools and smart habits, helping you stay ahead financially.

Explore trusted services today to get started on monitoring your score.